Economic ideologies have shaped the course of history, influencing governments, societies, and the way wealth is distributed. Understanding these ideologies is essential for grasping the fundamentals of economic theory and their real-world applications. In this article, we will explore Liberalism, Keynesianism, and Socialism, delving into their core principles, historical context, and modern implications. Let’s dive in! 🚀

What Are Economic Ideologies?

Economic ideologies are systems of thought that define how economies should be organized and managed. They provide a framework for addressing questions like:

- Who controls resources?

- How should wealth be distributed?

- What role should the government play in the economy?

Let’s examine the three major economic ideologies in detail.

1. Liberalism: The Ideology of Free Markets

What is Liberalism?

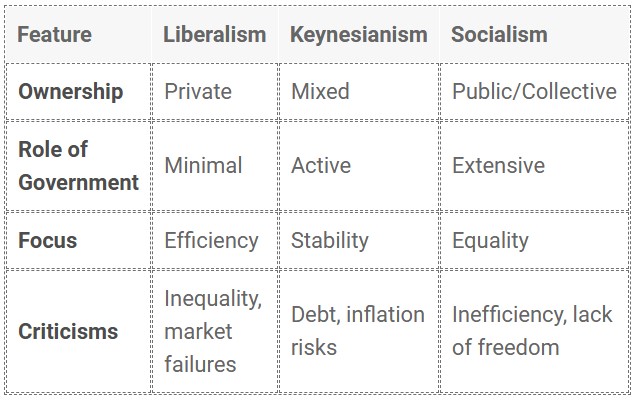

Liberalism is an economic ideology rooted in the belief that individual freedom and free markets lead to the most efficient allocation of resources. Originating in the 18th century during the Enlightenment, liberalism advocates minimal government intervention in the economy.

Key Principles

- Free Markets: The economy functions best when supply and demand are allowed to operate without interference.

- Private Property: Individuals have the right to own and control property.

- Limited Government: The state’s role is to protect property rights, enforce contracts, and maintain order.

- Competition: Encourages innovation, efficiency, and better consumer choices.

Historical Context

The ideas of Adam Smith, often considered the father of modern economics, are foundational to liberalism. His 1776 work, The Wealth of Nations, introduced the concept of the invisible hand, suggesting that individuals pursuing their own interests inadvertently benefit society as a whole.

Liberalism became the dominant economic ideology during the Industrial Revolution, driving rapid economic growth but also sparking debates about inequality and workers’ rights.

Criticisms

While liberalism promotes economic efficiency, it has been criticized for:

- Income Inequality: The rich often accumulate more wealth, exacerbating social disparities.

- Market Failures: Free markets can lead to monopolies, environmental degradation, and economic crises.

Modern Applications

Liberalism continues to influence policies emphasizing deregulation, free trade, and globalization. Organizations like the World Trade Organization (WTO) and agreements like NAFTA are rooted in liberal economic principles.

2. Keynesianism: Balancing Markets with Government Intervention

What is Keynesianism?

Keynesianism emerged in the early 20th century as a response to the Great Depression. Developed by John Maynard Keynes, it emphasizes the role of government intervention in stabilizing the economy and promoting growth.

Key Principles

- Government Intervention: Active fiscal and monetary policies can mitigate economic downturns.

- Aggregate Demand: Economic growth is driven by consumer spending, business investment, and government expenditure.

- Counter-Cyclicality: Governments should spend more during recessions and save during booms.

Historical Context

During the 1930s, the global economy was in turmoil. Traditional liberal policies failed to address mass unemployment and economic stagnation. Keynes’ The General Theory of Employment, Interest, and Money (1936) revolutionized economics by advocating for increased government spending to boost demand.

Criticisms

Although Keynesianism has been highly influential, it faces criticism for:

- Deficit Spending: Excessive government borrowing can lead to high national debt.

- Inflation Risks: Stimulus measures may overheat the economy.

- Political Challenges: Governments may struggle to reduce spending during economic booms.

Modern Applications

Keynesian principles have shaped policies like:

- The New Deal in the United States during the 1930s.

- Stimulus packages during the 2008 Financial Crisis and the COVID-19 pandemic.

Central banks also employ Keynesian tools like adjusting interest rates to influence economic activity.

3. Socialism: Prioritizing Equality and Collective Ownership

What is Socialism?

Socialism is an economic ideology advocating for collective ownership of resources and wealth distribution based on need. It seeks to reduce inequality and ensure that economic benefits are shared more equitably.

Key Principles

- Public Ownership: Major industries and resources are owned and managed by the state or communities.

- Economic Planning: Centralized planning replaces market mechanisms to allocate resources.

- Social Welfare: A strong safety net ensures access to healthcare, education, and housing for all.

- Equality: Reducing the gap between the rich and poor is a primary goal.

Historical Context

Socialism gained traction in the 19th century as a critique of industrial capitalism’s exploitation of workers. Thinkers like Karl Marx and Friedrich Engels laid its foundations, particularly in The Communist Manifesto (1848).

Various socialist movements emerged, ranging from democratic socialism to revolutionary communism. The 20th century saw socialism implemented in countries like the Soviet Union and China, with varying degrees of success.

Criticisms

Socialism is often criticized for:

- Inefficiency: Centralized planning can stifle innovation and lead to resource misallocation.

- Lack of Incentives: Equal outcomes may reduce motivation for individual effort.

- Authoritarianism: In some cases, socialist regimes have suppressed political freedoms.

Modern Applications

Today, socialism is evident in policies such as:

- Universal healthcare and free education in many European countries.

- Worker cooperatives and public ownership of key industries.

Countries like Sweden and Norway combine socialism with market mechanisms, creating hybrid models often referred to as social democracies.

Comparing the Ideologies

Which Ideology is Best?

There is no one-size-fits-all answer. Each ideology has its strengths and weaknesses, and their effectiveness often depends on the specific context of a country or region. For example:

- Liberalism thrives in innovation-driven economies but struggles with inequality.

- Keynesianism is effective during economic crises but requires careful management to avoid debt.

- Socialism reduces inequality but may hinder economic dynamism.

Most modern economies adopt a mixed approach, blending elements of these ideologies to balance growth, stability, and equity.

Conclusion

Understanding liberalism, Keynesianism, and socialism helps us appreciate the diverse approaches to managing economies. Each ideology offers valuable insights and tools for addressing economic challenges. By learning from their principles and history, we can craft policies that foster prosperity, fairness, and resilience.